Today, companies require industry-specific supply chain solutions. The performance of 82% of the industries–I term this industry potential–is going backward while companies are trying to push supply chain improvement. Most supply chain leaders are unaware they are facing an uphill battle. There is waste in the value chain that goes untapped.

We have automated enterprise supply chains not value networks. Many times a well intended consultant will generalize and minimize the importance of industry-specific functionality. Please note that any methodology that puts all companies into a spreadsheet — while losing the industry nuance — should be thrown in the nearest trash can.

The goal of this post is to focus the reader first align on the differences and potential of each industry and then make a plea for supply chain leaders to build value networks.

Learning From The Supply Chains to Admire Methodology

I am deep into the Supply Chains to Admire Analysis. The report takes me three weeks to write (after Regina spends 18 weeks pulling and analyzing the data). It is always interesting for me to see the emergence of industry patterns.

This year’s analysis is particularly interesting because it spans 2016 to 2025. (We have been looking at ten-year comparisons of the industry since 2013.) The reason? It takes companies an average of four years to drive substantial supply chain improvement. Three years pre-COVID and three years post-COVID yields valuable insights on resilience.

The typical manufacturing company grew 2.8% annually before COVID, but the discrete industries rebounded post-COVID due to war, shifts in technology platforms, and the growth of Artificial Intelligence (AI). Process-based companies, with the exception of pharma, were stalled.

In the report, I separate process-based manufacturing companies from discrete ones. The difference? Process-based companies predominantly focus on make-to-stock processes, while the discrete industries are more focused on configure-to-order or make-to-order processes. In the past decade, technologists have focused more on automating process-based manufacturing and underserved the discrete industry. This is despite the larger market potential in the discrete industries.

The Supply Chains to Admire report analyzes companies within an industry and rewards companies that drive improvement faster than the peer group at the intersection of operating margin and inventory turns while outperforming their peer group on growth, inventory turns, operating margin, and Return on Capital Employed. Why these metrics? Based on 10 years of research, first with Arizona State University and more recently at Georgia Tech, these metrics, when combined, can predict value as measured by market capitalization/employee. I want to help companies move from a cost-based agenda to one driven by value. This is my goal.

Measuring Industry Performance

In Tables 1 and 2, note that each industry has a different pattern. The largest companies by both revenue and market capitalization/employee are in the beverage, household durable, medical device, pharmaceutical, and semiconductor industries.

The interesting thing to me about this analysis is that for the past two decades, we have not achieved the supply chain economy of scale. As you will see from the report’s release on June 23rd, small companies that are more focused on innovation in a well-defined peer group consistently outperform larger companies. For example, Church & Dwight outperforms P&G; Monster Beverages outperforms AB InBev, Coca-Cola, or PepsiCo; and Ecolabs outperforms BASF or Dow. This is despite the industry’s commonly held beliefs that these larger companies are the market leaders.

What did I learn from the analysis so far? Here I share early insights:

- Improvement and Performance are Different Patterns. When companies start their journeys to drive performance it is easier to drive a difference. As companies mature, it is more difficult. Top performers like L’Oreal, Nike, and Somnigroup outperform in their sectors, but struggle to sustain improvement. When you reach higher levels of performance, it takes a step change to continue to drive improvement.

- Functional Metrics Erode Performance. Companies with deep investments in manufacturing scheduling underperform because the strong focus on manufacturing efficiency throws the supply chain out of balance, increasing inventory levels and reducing operating margins. A strong reminder that the supply chain is a complex, non-linear system. When companies optimize for a single function, they reduce value as measured by market capitalization per employee.

- Perception is Not Reality. The public perception of top performers could not be more wrong. Most industry conference keynotes are large companies that are underperforming.

- A Need to Rethink First Principles. There is no new normal. Post-COVID, the name of the game is not process improvement based on yesterday’s technology or process definitions. The business requirements changed at a first-principle level. Now, the goal is redefining processes based on new operating models using market data.

Table 1: Process-Based Manufacturers

Table 2: Discrete Manufacturers

Leadership Vacuum

I find it interesting that no company with an operating margin above 15% and a dominant position in its value chain has pushed the industry build a value chain and crack the code on building network interoperability. The supply chain, sadly, after four decades, largely operates on spreadsheets and EDI. The efforts at digital transformation failed because the focus was on automating historical practices, ignoring that each industry has shifted to a fundamentally different operating model. There is a glaring need for value-chain leadership. I am fearful that we will put AI on top of a system that requires change.

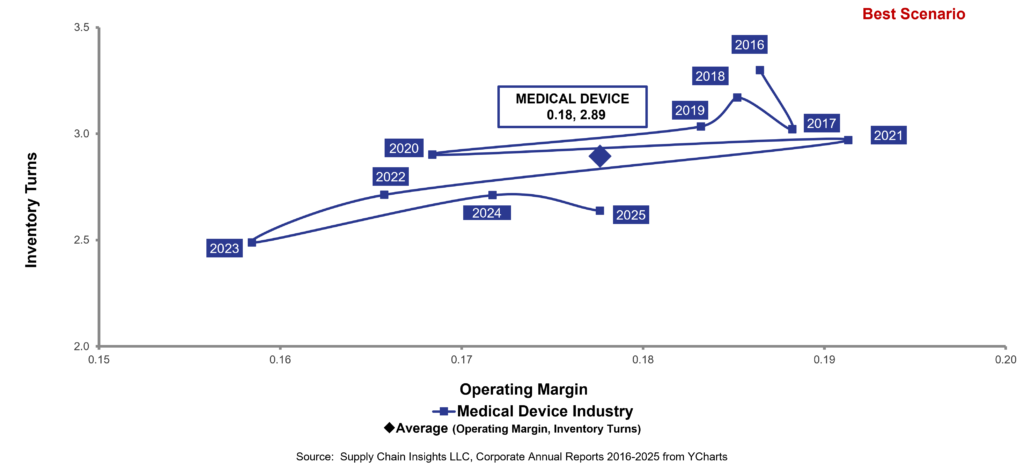

To understand the dilemma, check out the pattern of the Medical Device industry with 19.1% margin. The industry performance deteriated from 2016 to 2023, but started to rebound in 2023. The inbound supply chain of procurement to manufacturing is still largely manual. Linneage and quality of conformance are opportunities. Now would be a good time to rethink supply chain fundamentals and build meaningful networks.

Figure 1. Orbit Chart for the Medical Device Industry 2016-2025

But, as I look at the current waving of hands of putting agents on top of APS or ERP by technology marketers to drive the autonomous supply chains, I know that teams are fighting an uphill battle. My goal is to put an arrow in the quiver of supply chain leaders to drive home the point that the change is necessary.