Hooey /foo͞′ē/: noun

- Nonsense.

- Silly talk or writing; nonsense.

Phooey /foo͞′ē/: interjection

- Used to express disgust, disbelief, or contempt.

- An expression of disgust, rejection, or disappointment.

For the last three weeks, I have been quiet. This post aims to shed light on a dark, automated world where supply chain leaders believe they have answers and are busy automating outdated processes, but not driving value.

The Prologue

I watched as supply chain retreads shuffled through the halls at the Gartner event, posting celebratory pictures on LinkedIn, and toasting their great accomplishments and group dinners. As I watch, I am struggling with Hooey: Phooey. Think of it as a diatribe of nonsense followed by my internal disgust.

My struggle? When you go to the home of an executive in the field of supply chain, opulence abounds. Lucrative compensation packages drive technology companies to close deals, but there is no accountability to drive value for the business client.

In parallel, the industry waxes eloquent about the benefits of AI, focusing on making current solutions faster or hands-free (less labor), but there is no clear industry definition of what drives value. Without a clear definition, the autonomous supply chain is just Hooey: Phoey.

What Is Value?

For the past decade, I have attempted to correlate choices made within the supply chain to the delivery of value. Each year, I write the Supply Chains to Admire report. As I watch all the nonsense on LinkedIn, I am deep in the analysis for the 2026 report.

One of my observations is that the generally held beliefs about top performers are false. My second observation is that the manufacturing companies touted as top supply chain performers and technologists who advocate for their solutions drive unsubstantiated promises.

To make my argument, let’s take a look at the chemical industry for the period of 2016-2025. The imbalance between supply growth and weaker global demand was a structural challenge by the mid-2020s that few companies navigated well. The industry went through three distinct periods of change:

- 2016-2019: Globalization and promise of digital transformation. Rise in focus on sustainability.

- 2019-2022: Faltering demand. Shifts in global consumption. Logistics constraints.

- 2022-2015: China’s expansion of chemical production capacity in petrochemicals, polyethylene, polyurethane, methanol, and commodity chemicals, creating downward pressure on prices and margins.

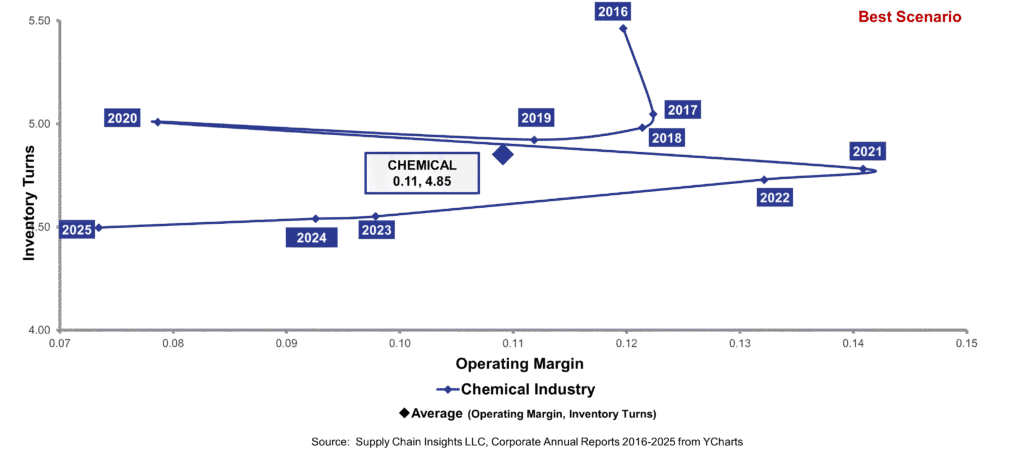

As shown in Figure 1, the investments prior to COVID — primarily in efficiency and inside-out processes — were deleterious to the companies to survive the shocks through and post COVID. The downward slide in margin potential at the intersection of operating margin and inventory turns with post-COVID capacity caught most by surprise.

Figure 1. Chemical Industry Orbit Chart 2016-2026

Digital transformation — over-hyped and under-delivered — by consultants and technologists lacked a common definition and value proposition. For many, it was a reason to continue spending on ERP and APS initiatives, assuming that historical definitions of supply chain excellence were sufficient. The focus was on manufacturing efficiency and improving internal processes to make data more available. These were faster and more capable inside-out processes, assuming that the order represented demand. Companies with the strongest focus on digital transformation underperformed.

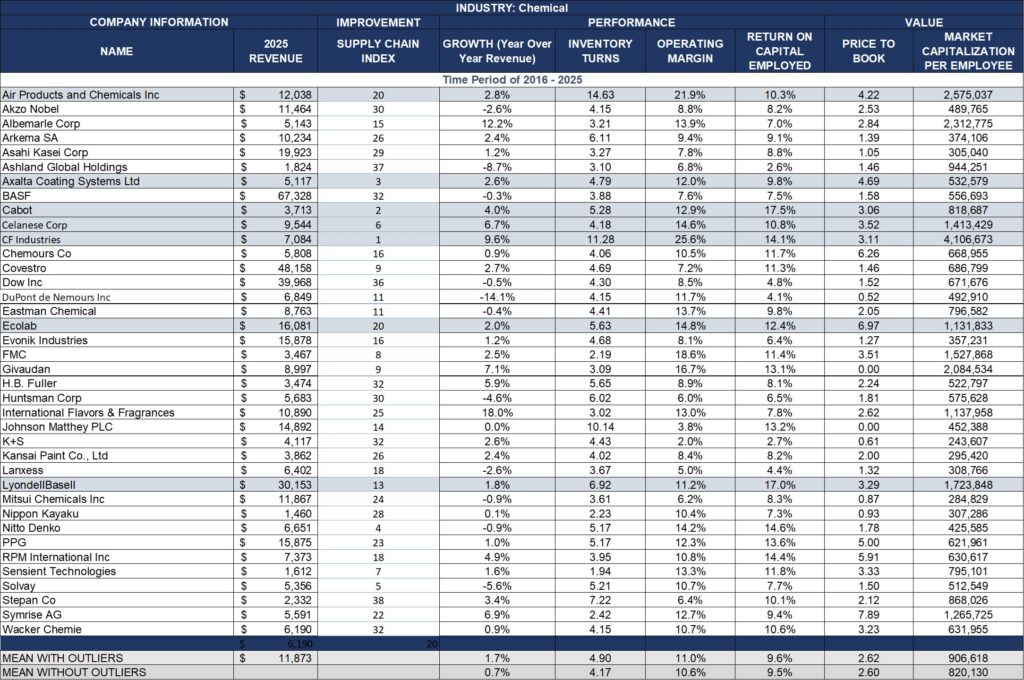

When you ask CHATGPT, which chemical companies are top performers, the answer is BASF and Dow, but this answer could not be further from the truth, as shown in Table 1.

Table 1. Supply Chains to Admire Analysis for 2016-2025

Here are my thoughts.

- First, look at growth. The market slump post-COVID caught most by surprise. Remember that supply chain teams do better when they are peddling uphill than downhill. A traditional focus on cost and manufacturing efficiency is a recipe for disaster when the industry enters a growth slump. The inside-out processes created a false sense of safety in a rapidly changing market post-COVID. Large companies were slower to respond than smaller companies.

- The larger the company, the more interconnected and the more automated it was, the poorer the performance. There was no substitute for leadership and functional alignment within the organization to drive performance.

- The industry’s perception of leaders and their actual performance are misaligned. BASF and Dow were not leaders during this period; yet, when you ask ChatGPT for the leaders in the chemical industry, they are rated highly. Each will likely make the Gartner Top 25 list based on popular opinion. Smaller players focused less on technology and more on organizational alignment through better management of feedstocks and go-to-market plans through S&OP, and delivered superior results.

- The fall of Eastman Chemical is particularly interesting to me. In 2015, Eastman was a winner of the Supply Chain to Admire Award. Today, the Company is a strong laggard, like P&G; it spends a lot of money not to grow. Eastman is the best deployment of OMP that I have witnessed, but the focus was on OEE and manufacturing efficiency with little interest in outside-in sensing. The company worked with Deloitte for many years on supply chain archetypes, but the driver was internal process improvement rather than market sensing or alignment. Let me ask, who cares if you can manage inventory if you cannot drive growth in a volatile market? The chart is a testimony to how spending a lot of money on traditional supply chain processes can lead to failure for shareholders, employees, and customers.

Can We Dispense with the Hooey?

Supply chains, to me, are serious business. As I watch friends at DOW be laid off, I cringe. I remember the Accenture ads at airports highlighting their success. You don’t see these same ads now.

When I see OMP touting the success at Eastman Chemical, I have to refocus and talk to the inner Lora not to write a diatribe about the dangers of inside-out processes in a volatile world. The sad thing is that most supply chain leaders believe that traditional processes are sufficient. Or that traditional demand planning is the key to success. Failure should be the reason to change, but the rich reward systems for technologists drive industry resistance.

So, can we dispense with the Hooey? Can you join me in the Phooey? Let me explain what I mean. Last month, Knut Alicke vibe coded to produce S&OP software in 30 hours. Madhav Durbha postulated on three layers of Context Engineering. Do we really care? What is the value to business leaders?

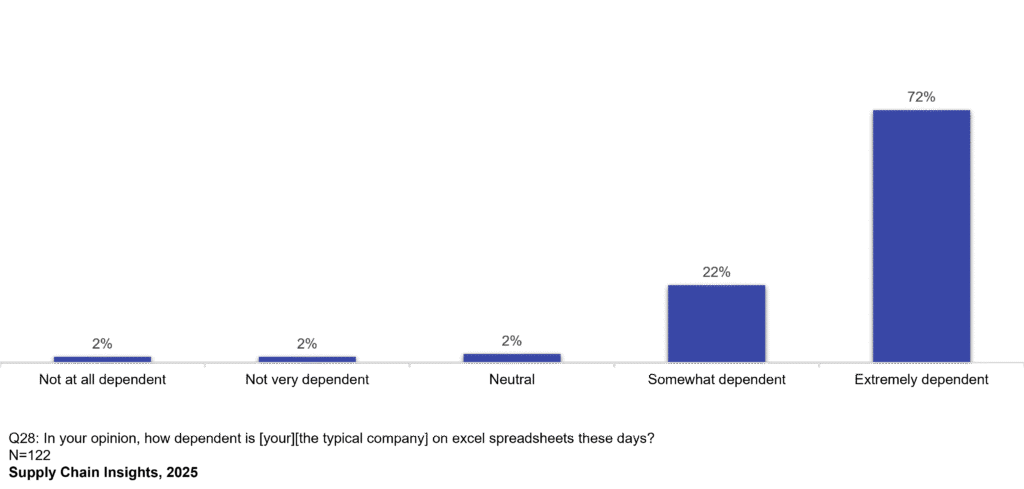

The problem is that existing process definitions and understandings are not sufficient. It does not matter that we can build code quickly if it is not used. I would like to see us start with a deeper understanding of user personas and gaps to explain why the Excel Spreadsheet is the number one supply chain planning technology.

Figure 2. Use of the Excel Spreadsheet in Supply Chain Planning

When KettieQ posts that planning is no longer a function, but a Continuous Decision System, I have a violent reaction. The blog post postulates that planning is moving from static outputs to continuous, agent-driven decisioning. It is no longer about creating a plan. It is about running a system that adapts in real time.

My fingers want to type violently, ENOUGH! I want to ask what decision intelligence is. While it is used frequently in marketing messages today, the buyer needs to ask. Is decision intelligence insight? Prediction? Recommendation? Decision? Course Correction?

When business leaders speak of the autonomous supply chain using traditional supply chain views, I envision a WAYMO car falling off the cliff, like BASF, Dow, and Eastman in the analysis above. Trust me, these were not dumb and uncaring teams. Instead, the focus was on the painful implementation of today’s processes, but it did not help, because inside-out processes are inadequate in a volatile world environment.

Can someone build an app quickly? Sure. But is it scalable? What about security? Future roadmap and product development? Software maintenance? Does your team really have the deep domain knowledge and technical expertise? Will the team use it? But, most importantly, will it drive value? Hooey, I say to all. My simple brain is trying to unravel the logic behind:

- Why are we trying to make today’s planning processes faster when they don’t work well? Why do 94% of companies with a supply chain planning system have a strong dependency on using Excel as their primary technology for planning?

- What good is software if it is not used to drive value? Why would we vibe code existing applications? A focus on cost degrades value.

- How can we run a system that adapts in real time if we are not clear on value-based outcomes? And, how to make the trade-offs across source, make, and deliver bidirectionally? Why are we not measuring the impact of waste and the bullwhip?

- Planning should never be real-time. Anyone who talks about real-time planning does not understand planning.

Instead, my focus is to prototype models that can create value. Here are my top four areas of focus. I want to sidestep HOOEY/Phoey by building prototypes with innovators:

- A Plan of Plans. My vision is that, as the ease of use and speed of network design tools rise, we can run different market scenarios before each S&OP review and then consume plans (not data, as is conventional thinking) as the market becomes clearer. Like a hurricane hitting Florida, in the strategic planning horizon, there would be 10-15 plans, each with a different probability. As the tactical horizon becomes the focus, the organization would work with the probabilities of different scenarios in the operational and executional environment. The focus is not on a single plan or probabilistic outcome of an engine; instead, the driver is tracking and analyzing different market scenarios.

- Demand Stream Management. Traditional demand management processes are flawed. Most assume that all items are forecastable, and there is no distinction in the alignment of demand and supply by stream. In each organization, there is an efficient product flow — that is, very predictable and manageable by conventional thinking — and the need for a responsive supply chain (short cycles) and an agile supply chain that is lumpy and unpredictable. The focus on FVA by stream and the inclusion of plans uses the probabilities of market potential in each scenario.

- Bi-directional Orchestration. Each industry needs to make trade-offs amongst make, source, and deliver to a balanced scorecard. Conventional processes focus on linear flow, recognizing manufacturing only as a constraint, and prioritize functional outcomes. This is problematic for many reasons.

- A Network of Networks. We need to leverage AI advancements to build a network of networks. Companies today lack interoperability among networks. Investments in control towers showed no value because most were insufficient in scope.

What Is Value?

Thanks for reading my blog.

I hope that you will join me in questioning traditional approaches to supply chain management that I believe are woefully inadequate for the global multinational. Instead of hyping the false promise of using Artificial Intelligence (AI) to automate traditional planning processes, I hope you will join me in pushing to use new technologies to redefine the promise of supply chain planning and drive value.

Enough Hooey: Phooey, I say. Supply chain excellence should be serious work to drive value.