Over four-hundred days of war in Ukraine. Growing tensions between China and trading partners. Unrest in Sudan. The global supply chain is built on three assumptions: rational government policy, availability of reasonably priced logistics, and low variability. In March 2023, the Global Supply Chain Pressure Index fell to the lowest level since November 2008. While many might clap their hands and exclaim the end of three-years of unprecedented supply chain disruption, I say, “Not so fast.” I feel like we are riding a gondola in the middle of an intense snowstorm. The ride is uphill, but the visibility is low.

What is normalcy? Yes, we have achieved greater normalcy in transportation. As consumer spending fell, the days of escalating ocean freight and extreme shipping variability eased this year. In the spring of 2022, Asia/US ocean container rates resumed pre-pandemic levels and congestion eased in November 2022 into California ports. However, variability and global unrest is rising.

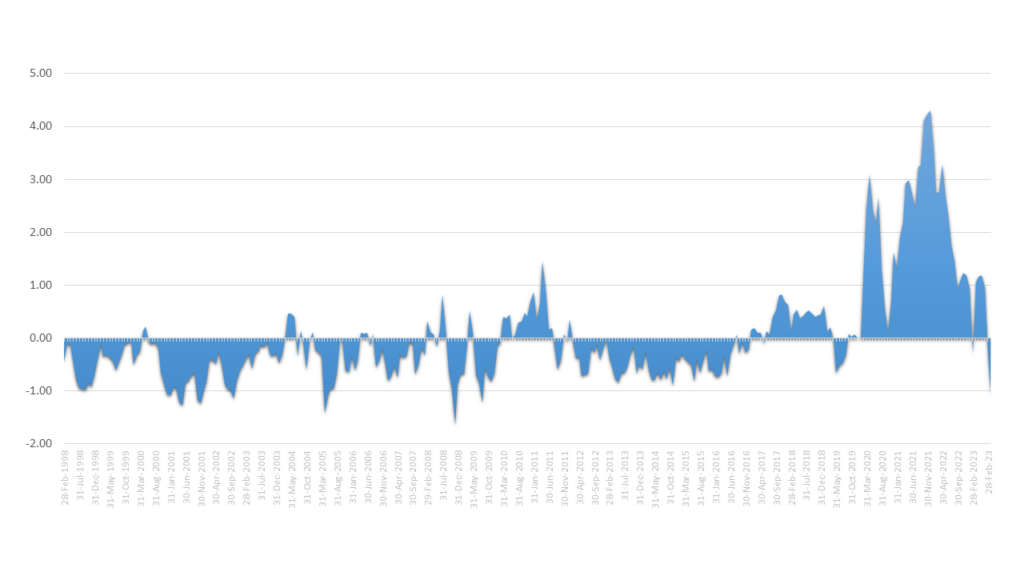

The peak disruption was in December 2021. In March 2023, the level of disruption fell to a level seen in November 1998.

Figure 1. The Global Supply Chain Pressure Index

With mounting inflationary pressures, challenges continue. Cash is king and financial viability is the overarching goal. The most significant factor to improve resilience (the organization’s ability to drive reliability of business results in the face of variability) is organizational alignment. While consultants wave their hands and tout new approaches, the most important step that a business leader can take today to improve future performance is the development of a shared vision for the organization on supply chain excellence. For organizations layered in functional metrics and driving a cost agenda, this is a tough nut to crack. Tougher than most understand.

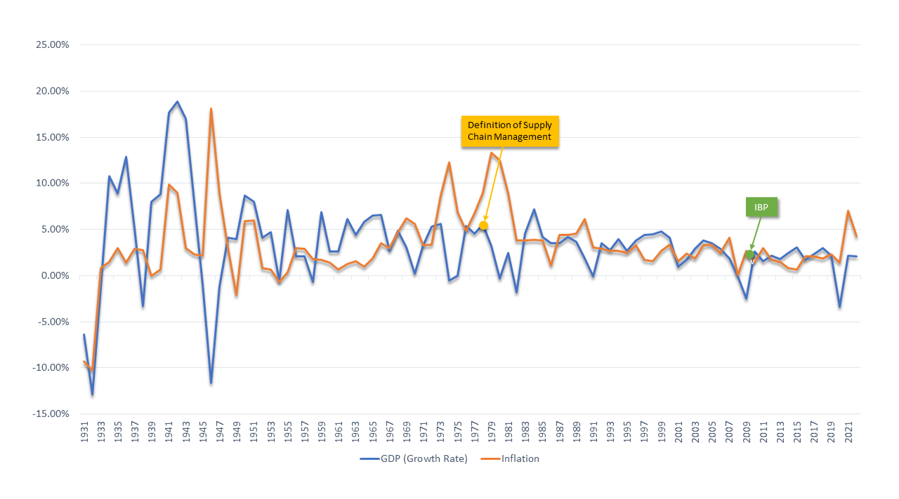

Figure 2. United States Inflation Rates and GDP

Challenges

Traditional definitions of supply chain excellence focus myopically on cost but are too slow in making decisions in inflationary periods. Companies need quicker answers with better insights, but current organizational processes are slow, putting supply chains on the back foot. During the pandemic, companies struggled with planning systems turning off the optimizers, and using the technology as a system of record.

- S&OP is too slow and cannot achieve the needed alignment. Process latency, the time for an organization to make a decision using a traditional S&OP process, is two-to-six weeks. In the face of variability, this is two-to-six weeks too long to make allocation or procurement decisions.

- Shift in cycles. Need for design. The traditional leader values cost reduction but is blind on how to value time. Over the past three years, supply chain cycles shifted. Currently, the cycles are out of balance. Order cycles–the requested time from order to delivery–decreased while supply cycles –the time to procure materials– increased. E-commerce models exacerbated this trend while supply variability challenged order reliability.

- Higher variability. Demand and supply planning processes assume low variability and use history as a guide in planning the future. However, today, supply chains are untethered. History is a poor guide for the future. The order is a poor proxy for demand. To side-step this issue, build planning processes to use market data. Abandon the processes focused on multiple layers of meetings to improve collaboration of organizations that are not aligned, but focused on transactional data.

- Bloom off the rose on digital transformation. The answer is not digital transformation. In the survey, 48% of companies were driving digital transformation, but the only element that improved performance was descriptive analytics. Companies driving digital transformation did not outperform their peer groups during the past three years. The reason? Digital supply chain transformation is over-hyped with a lack of clarity on value. The central problem is the lack of a clear roadmap to define core capabilities.

Steps to Take

Here are three steps to take:

- Build adaptive modeling. Align the organization and focus resources on building adaptive modeling capability. (I don’t care what you call it, but network design, what-if analysis, simulation and digital twin approaches grow in importance.) Train teams to model variability and build a planning master data layer to understand layers of variability. (A planning master data layer measures and tracks shifts in lead times, conversion rates, and quality. Feed the adaptive modeling environment market planning master data.)

- Side-step large-scale digital transformation projects. Digital supply chain projects never achieved promise. In this time of variability, focus less on hype and more on pragmatic delivery. Show the technology vendors touting digital and AI transformation the door. (Yes, better optimizers are a blessing, but now, focus small to visualize and align on alternatives.)

- Build in-market sourcing. Make divisions and regions self-sufficient. Rationalize global strategies to focus on building markets based on in-market sourcing. Align the organization to a balanced scorecard approach and use adaptive modeling to drive discussions cross-functionally. Actively design supply chain flows (not just assets) on a quarterly and monthly cadence. (I find that it is easier for organizations to align when they see the impact of a model and have the ability to fine-tune and see alternatives.) To accomplish this goal avoid hardwiring planning platforms to transactional systems.

What Is the Value of A Network?

I continue to hope that organizations will get more serious on building networks. Currently, I am working on a study to understand the value of synchronizing contract manufacturing with in-house manufacturing and procurement. Today, companies believe that network relationships are essential, but most funding goes to investments in enterprise investments. The average brand owner outsources 28-35% of manufacturing, but most coordinate using only spreadsheets and email. Automation is an opportunity, but what is the value? This is what we are trying to assess.

Interested? We would love to have you participate in a study to understand the current state, the value of automation, and the business drivers. If you click the link, please be assured that all responses are reported in aggregate, and the names are anonymous. Companies participating get a copy of the results.

About the Global Supply Chain Pressure Index (GSCPI): The GSCPI integrates a number of commonly used metrics to provide a comprehensive summary of potential supply chain disruptions.